#1 The Latvian story - inflation & interest rates

#1 The Latvian story - inflation & interest rates

❄️ Is the winter finally coming? Let's take a look on the inflation and the ECB interest rates through the eyes of a Latvian. Is the situation just fine or getting scary?

👋 Brief intro

The summertime is warming up & you are planning your long-awaited vacation, thinking about those warm evenings with a cold beer & great friends around. Yet.. the world might be setting a scene for some potentially very cold headwinds (also literally) during the coming Autumn & Winter. The winter might really be coming.

There are many interesting reads, podcasts & views globally, but for me, we are lacking local analysis of our Latvian case. I will try to make sense of it in writing as it also helps me to put everything in perspective.

I love examples & some data, so you will see a fair amount of those.

Read responsibly as this is being written only as speculation & I am no expert in all of these fields so there is no need to take me too seriously. However, I am more than interested in discussing any of the topics in more detail & hearing your thoughts - be they the same or different. I am just scratching the surface here & not doing an in-depth analysis.

Topics to be covered during the saga

This will be a saga on the cause and effect relationship (*read in Dalio’s voice*) between multiple things that are happening in the world & that will have larger or smaller effects on everyone.

Some of the topics:

💸 Inflation remains high & it has yet to be addressed

🏦 Interbank lending rates get ready for lift-off

🔮 Other things & speculations (this one will be updated periodically)

I will also try to give you some practical tools to better understand your personal case.

💸 Inflation remains high & it has yet to be addressed

Inflation is probably THE word of the year, therefore, I will not go into too much of an explanation - inflation is % by which prices for stuff go up compared to the same period 12 months ago.

Before we go into more details, let’s meet our persona who will be a great help for looking at examples:

Matīss (33) is just a regular everyday guy who earns an above-average salary of EUR 2k net (after-tax). Has a dog, is not married yet, but has met the wonderful world of liabilities by taking a couple of loans. More on that later.

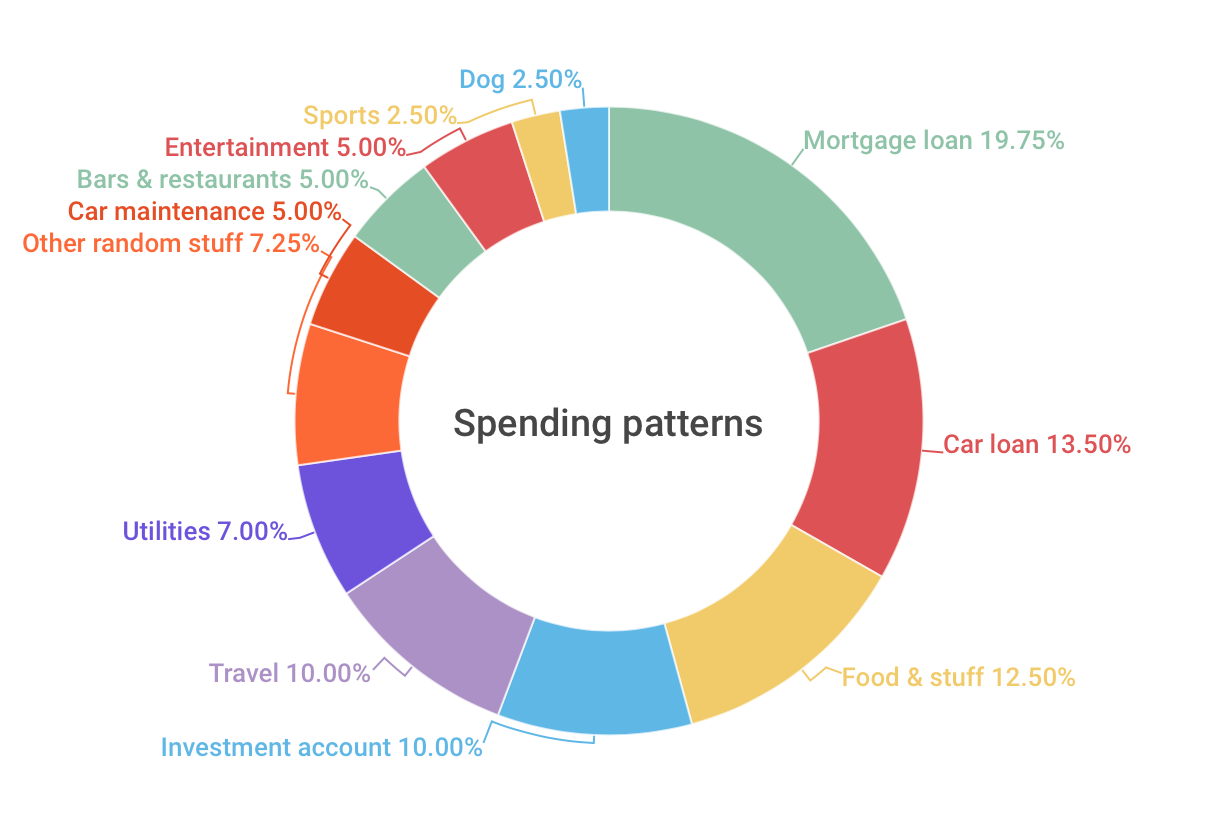

It might be useful to define his regular average monthly spending patterns & savings in 2021:

Here goes the same spending patterns in writing:

Mandatory payments | 60% | EUR 1,205:

Liabilities (33%):

Apartment loan: EUR 395

Car loan: EUR 270

Food & stuff for home (12.5%): EUR 250

Car maintenance & gas (5%): EUR 100

Utilities, incl. electricity (7%): EUR 140 (EUR 40 electricity)

Dog (2.5%): EUR 50

Somewhat optional | 40% | EUR 795:

Investment account (10%): EUR 200

Travel (10%): EUR 200

Other random stuff (7%): EUR 145

Bars & restaurants (5%): EUR 100

Entertainment (5%): EUR 100

Sports (2.5%): EUR 50

And savings:

The investment account (stocks, some crypto) has done pretty well soaring to EUR 6,420.

Cash position of EUR 3,580.

EUR 10k altogether.

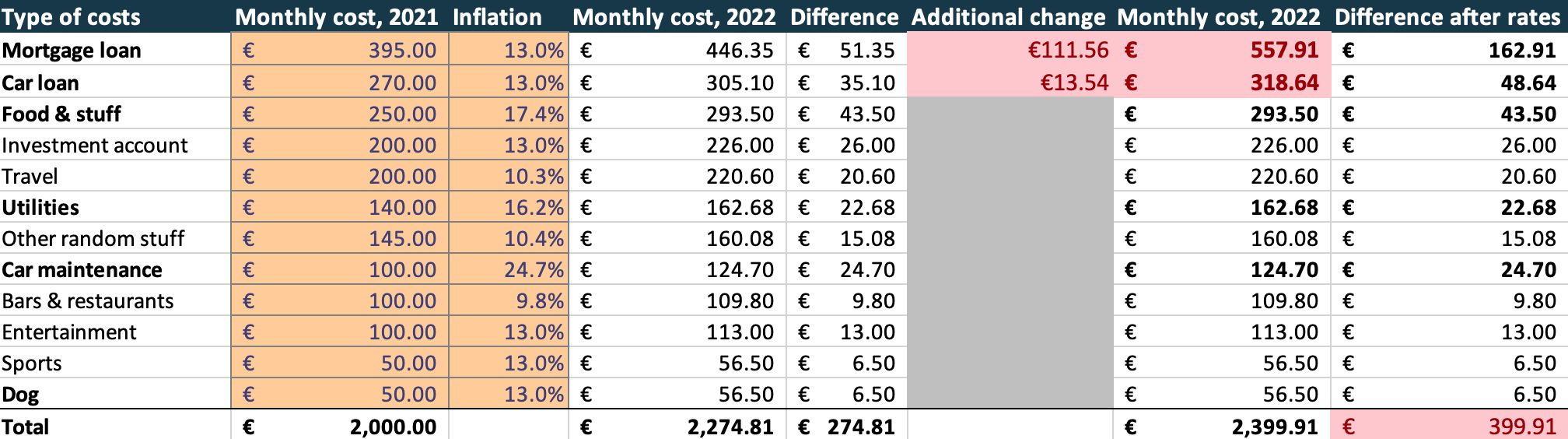

The last reported inflation number was 13% for the month of April, but let's use somewhat right number for the specific positions and see how it goes for Matīss.

On average, Matīss has lost around 13% of his purchasing power & we can effectively take this 13% away from his income which means that his real purchasing power is now EUR 1,725 compared to last year's EUR 2,000. EUR 275 just vanishes. Or looking at it from the other side (like in the table below) his missing EUR 275 to sustain the same way of living.

His savings also got a hit:

I would say that the investments are somewhat ok in terms of inflation (unrealized gains/losses are still unrealized), but there are other issues. More on that later in the part “🩸 Markets are bleeding”, but I guess you know where am I going with this.

Cash position's actual worth goes down by the average 13%: EUR 3,580 - 13% = EUR 3,115

I am no Nostradamus, but I would put my money on the fact that Matīss is not cutting his travel budget just yet (probably just went to Finland for hockey championship) & entertainment is also entertaining. So probably, ok unlikely but possible, just trying to cut something from the “Other random stuff” category & putting some short-term halt to feeding the investment account. Maybe just taking the cash out of savings.

Matīss is still fine & mostly does not notice the changes, just casually mentioning the raising prices over a beer with friends and to his dog during the walks.

🏦 Interbank lending rates get ready for lift-off:

Interbank lending rates will be going up with the European Central Bank’s reference interest rates. ECB has just given somewhat clear guidance on this. The rate will go up to 0.5% already in September and I would speculate that it’s not stopping there. These are the rates for which the banks lend funds to each other & they are commonly called Euribor which is short for Euro Interbank Offered Rate.

So what does it mean & is it really the only way to stop the prices from going up (inflation)? Well no, but typically, this is the way - whenever inflation starts to pick up the central banks react by raising the rates & the logic is pretty simple - the higher the borrowing rates, the less likely that people will borrow some additional money & spend it. Put it simply - less money around —> increased competition between companies selling stuff —> cheaper stuff or at least not more expensive —> slowly back to normal. Nonetheless, this is not a perfect formula and a lot can go wrong as the less successful companies get hurt and subsequently their employees and so on, yet it makes sense in long term as per survival of the fittest.

As you can see in the chart below - inflation was even higher back at the end of 2007 / early 2008 & part of you might remember how much not fun the next years with the global financial crisis were. Unemployment >20%, mass emigration out of Latvia & all the austerity measures by the government.

Back then the rates went from 2%—>5%, so a 3% increase in a couple of years, somewhat similar to the early 2000s with the dot.com bubble.

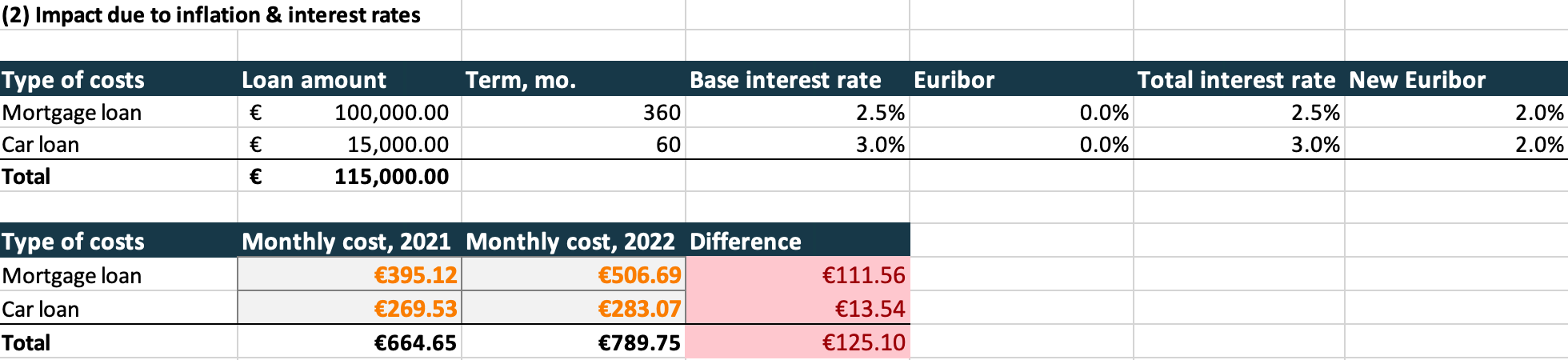

Ok, sure, but what does it mean for me & more importantly for Matīss? These higher rates will be passed over (obviously) to the consumers, read YOU. Do you remember that weird Euribor rate that I mentioned previously and that has been irrelevant for years, well it's also mentioned in your loan agreement. Aaand.. it won't be that irrelevant for the years to come. Let's take a look at a simple example.

Going back to our friend Matīss who earns EUR 2k net (after-tax) that has now actually gone down to EUR 1,725 due to inflation. He has two loans for a car & an apartment & let’s assume that the Euribor goes up to 2%. I believe that 2% is definitely not extreme & could happen in 12-24 months (my personal feeling only), the highest values were 5.2% & 5.4% back in 2000 & 2008, respectively.

Car loan (finance lease): 5 years, EUR 15,000, base interest rate 3% + Euribor rate (6m).

Now: EUR 270 monthly

Then: EUR 283 monthly

Monthly increase of EUR 14, meh.

Home loan: 30 years, EUR 100,000, base interest rate 2.5% + EURIBOR rate (6m).

Now: EUR 395

Then: EUR 506

Monthly increase of EUR 111, Matīss sad.

Matīss liabilities just increased by EUR 125 or 7% of his purchasing power after inflation.

Again probably no biggy & Matīss is still fine (is he though?) as his base salary was well above-average, but let's go to summary to understand where does he stand as of now.

💭 Summary (with some additional data)

Inflation is near a record high & is likely to remain so for a foreseeable future. It eats around 13% (maybe more, maybe less in the future) of people purchasing power, meaning that people collectively become poorer.

To address the inflation issue, ECB will stop printing money (no, they have not stopped yet) and increase their reference interest rates. Interbank rates (Euribor) will be passed to consumers & effectively increase the money to be paid for debt, be it mortgage, lease, or anything else. Again, see Matīss example.

What has happened to Matīss and what will happen to people worse off?

Liabilities have gone up to 44% of his monthly budget, compared to 33% back in 2021. These are an extra EUR 211,55, adjusted to inflation. What happens is actually pretty sad with two negatives at the same time: (1) your money is worth less, (2) your liabilities are getting more expensive.

Due to inflation & interest rates, Matīss has got EUR 400 poorer on a monthly basis & lost EUR 465 of his cash savings.

If we take a look at mandatory (see in bold) vs somewhat optional categories, then mandatory payments have grown to EUR 1,457 or 76% of total purchasing power, compared to 58% in 2021. Does not sound too good to me anymore.

Yes, Matīss has a mortgage that has a large impact, and not all people have mortgages. However, all the people live somewhere & if the rates go up then part of the landlords could increase the rent if they have a loan in the bank.

Probably Matīss will be fine with some cost-cutting if he remains employed; however, as noted he had a very decent salary of EUR 2k net & no wife, kids, just his friendly dog that eats some EUR 50 per month.

If we would do this exercise (& I recommend you do it for yourself) with a person with a salary of EUR 1.2k, then the situation might get critical real quick.

If you take one thing from this jibber-jabber, then just: “Hope for the best but be ready for the worst”.

As said at the very beginning - I am more than interested in your thoughts.

Next up: “😵💫 Geopolitics landscape is uncertain, to say the least“, let’s see how that will impact our friendly sailor Matīss.

Yours sincerely,

Roberts L.

BoE hikes rates to 12 year high 1.25% https://uk.finance.yahoo.com/news/bank-of-england-uk-interest-rates-110248955.html

FED hiking another 0.75%

https://www.wsj.com/livecoverage/federal-reserve-meeting-interest-rates-june-2022