Knocking out the inflation

Knocking out the inflation

💸 Inflation is here, but isn't there really anything that we can do about it? I believe that anything is solvable & so is inflation! Anyone can improve their situation by doing just a few things..

👋 Brief intro

I hope that you are having a time of your life & not taking everything too seriously. The first part of our meeting might have been a bit soar with the thrilling Latvian story, but I kind of feel like it was necessary.

Now, it’s time for the fun as we tackle the inflation, give it a couple of punches & get to the solutions. I believe that anything is solvable. I mean look people invented electricity & the internet, got to the moon, lived through the Trump presidency & most importantly invented chips by putting slices of potatos in boiling oil (amazed).

With that in mind, I am sure that we can figure out how to fight the raising prices. What we gonna do is (a) imagine that your finances are an actual business, (b) play a game & (c) I will share my tips & tricks. It’s gonna be fun!

Btw, in one of the first articles I promised to share some workings - this is the time ☀️

🧮 Step 1 - understanding your situation

The return of the Jedi

Ok, now let’s assume that you are a business owner & you start to get the feeling that the shit is about to hit the fan badly. Something feels off. What do you do? You look at your numbers. As you might expect, then this is the time when we announce the return of our Jedi - Matīss & he will play the main role once again. Applause to him! (if you have no idea who is Matīss then go to my first article & meet him).

Btw, some of the readers have been asking whether Matīss does not have some friends that earn less as that would be interesting to see in examples - let’s see, I will ask him.

Helpful tools

I love tools, I mean like software tools, not actual tools (pretty terrible with the actual). And luckily for us, there are some that are very helpful with understanding our costs:

The basics - if your bank does not have a tool for tracking the spending, then please do change the bank. Revolut calls them analytics, N26 insights, Swedbank “Mans budžets“. I cannot vouch for Swedbank’s quality as I am not using their tool. The other two are decent.

My latest discovery - Spiir which is a bank account aggregator so you can see all your spending in one app + some analytics. Again - useful if you are using multiple cards/bank accounts; the best that I have seen & I am using it. They targeted me with an Instagram ad, so good job on their side.

I have an extremely large heart (& obviously hate bragging), so I have created & am sharing a google sheet that will do some dark magic for you. You can (read should) download it and use it for your unique case.

IMHO, these tools (or similar) are the basic hygiene that I believe anyone (young/old, poor/rich, doesn't matter) should be using, especially in more turbulent times. You gotta respect your future self.

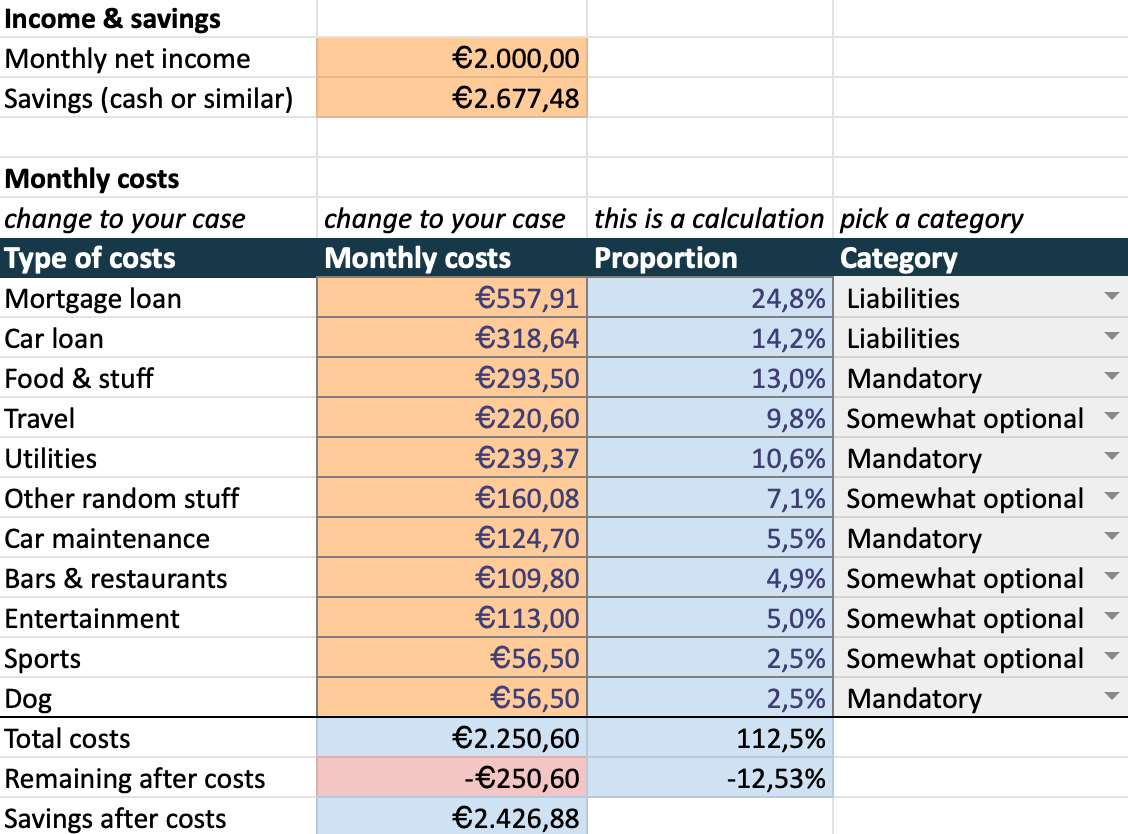

Just below are Matīss numbers after our infamous inflation (among other) adjustments & when you update your numbers you will have a similar summary. I've also added a pie chart to make it easier to visualize the costs. If you feel courageous enough, then you can share your pie with others in the comments section.

Introducing metrics

There are some metrics/indicators that I have added that felt worthwhile looking at:

Mandatory costs / all costs - to see how large is the part that is more difficult to be changed.

Debt to income - a popular metric for banks or any lenders to see the risk level of the borrower.

Cash runway - how many months do you have left until running out of savings, if you are burning money (overspending).

These will be especially interesting as soon as you start playing the game. 👇

🎮 Step 2 - playing the “take over control“ game

Ready Player One

I said that it’s gonna be more fun than it sounds, but ok, seriously this is the top level of my nerdiness. Now, if you opened my google sheet & if you are human, then you probably already checked out the sheet called “Take over control“ game.

May the odds be in your favor.

The game is pretty simple & the goal is for you to take over control of your finances. We will be focusing on your spending and different scenarios so that it’s easier to understand where do you actually stand. You will be able to adjust inflation, utility prices, your liabilities, etc. but really all you need to do is follow my comments & they will guide you through. I would suggest that you play around with the numbers & check out different scenarios - good, neutral & bad. Just an idea of how you could look at it:

Good - better job or an increase in salary, stable Euribor, no further increase in prices.

Neutral - same salary, Euribor in range of 1% - 2%, lower price increase 5%.

Bad - losing job/unemployment benefits, Euribor at 3%, inflation remains 15%.

Those are just some ideas to play around with, but feel free to mix them up for your own taste.

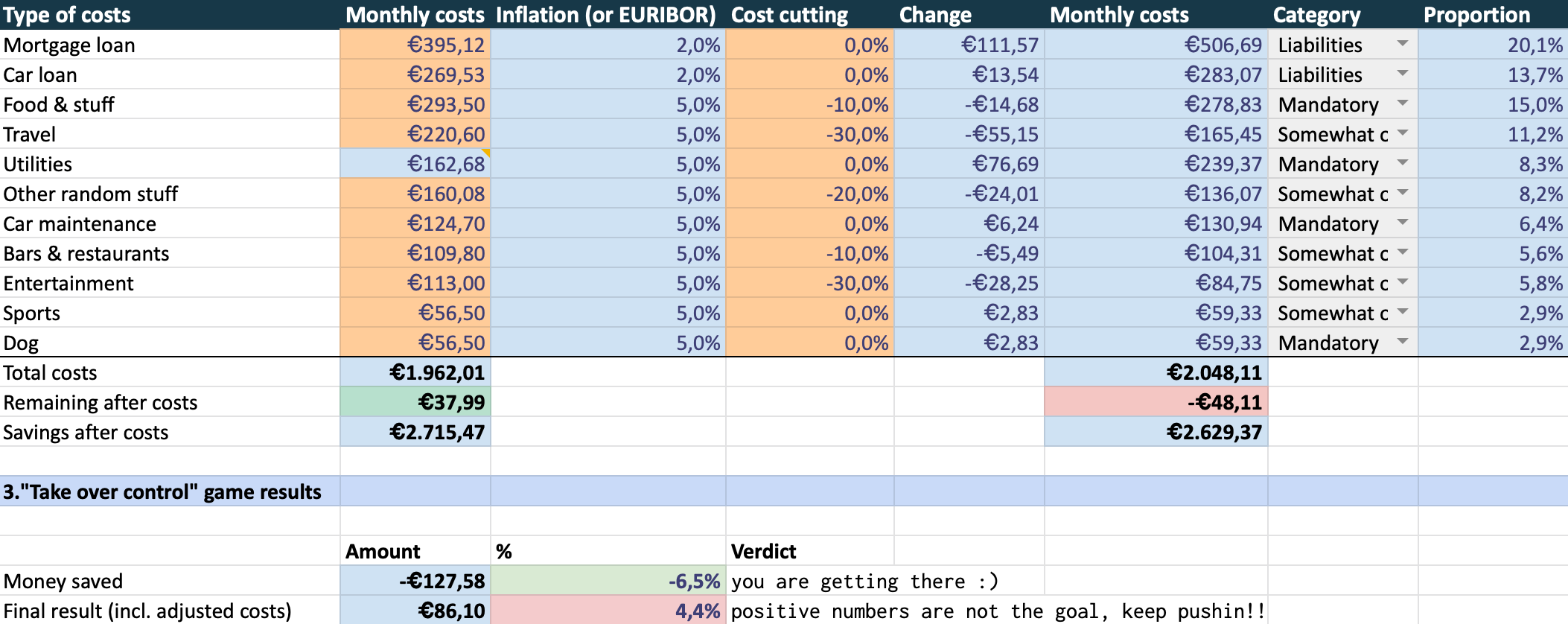

How did it play out for Matīss

The weirdness in the game (or life?) is the fact that even with some heavy cost-cutting you can still be worse off, if the inflation, Euribor, and other factors do not work in your favor. For example, just look at the picture below of the Matīss result.

If that is the case for yourself as well, then probably you are looking for some great additional ideas. I will try to help & let’s hope that other readers will share them as well.

🤌 Step 3 - hacking the inflation

#1 | Just don’t spend the money

As silly as it sounds, it actually makes sense even though it is very counterintuitive & against basic economic principle of time value of money. But you have to remember - we are in an extremely inflationary environment & current prices are not normal. Yes, the best answer might be some inflation hedged assets, but cash will be fine for most. I believe that we should not be acting like things are on discount when they are the other way around. Believe me, inflation will settle eventually & even if the prices remain elevated for some goods & services, then at least part of them will normalize and maybe even deflate.

If you have tried investing, then you know that in investing nobody wants realize the losses as you always hope for the stock to bounce back. Somehow it’s not the same with inflation when people try to to spend (realize) when the prices are up, but why?

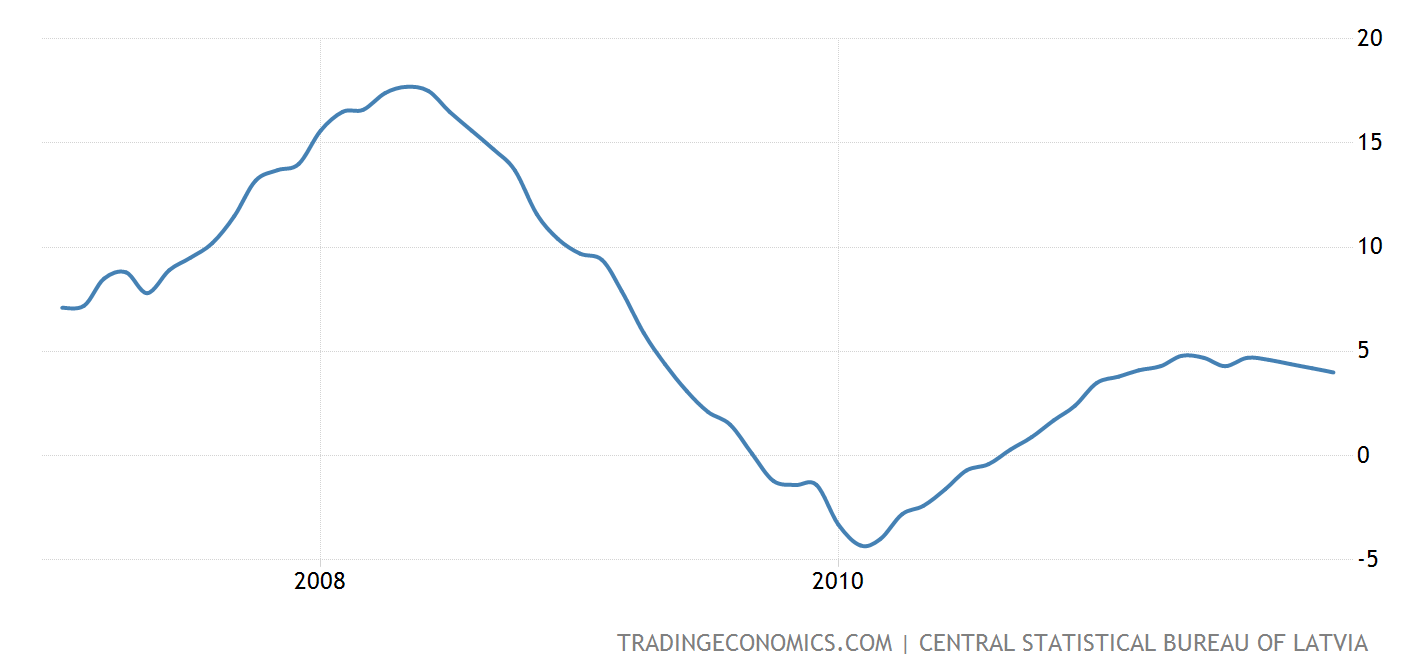

In my experience, money gives more peace of mind, and safety & lets you focus on other more meaningful things. Look at the graph below, this is inflation in Latvia during the 2007-2012 period. As of today, we might be near the peak of the current inflationary period and the numbers will probably start to go down during the next 6-12 months; give or take a couple of months. Before that though, we should brace ourselves for new record highs.

You might say, ok, but one event is not much of data & yes, that is true. U.S. data might be more interesting as they have longer history, but I will not go in great detail to save our time, just check the marked periods.

#2 | Go German

This one is an easy one - buy discounted stuff in bulk. I mean there is no shame in being smart & thoughtful. In May 2022, the inflation for food was 18.8%, so if you see something with 10% - 20% discount & you know for a fact that you will need it, then just go for it. Don’t go crazy though, as that contradicts the #1 point just above.

#3 | Ok, but what to buy?

If you have got through this point, then you have definitely earned some tips based on Latvian inflation statistics, here we go:

Food:

If you buy meat, then go for pork. Inflation just 7.9%. For comparison, poultry (bird meat) is dominating with 33.6%. Chicks.

Fish - well, not great, everything apart frozen seafood (15.4%) is at least 20% up. Go fishing.

Another crazy one is pasta (🍝) with 38.8%. Kind of feels like they are going after me.

It seems like eggs is the way. Only 12.5%. While milk is up 31.2%. Looks like I will have to change my pancakes recipe.

Fresh or dried fruit is another hidden gem with inflation of 7.2% and 6.3%, respectively.

Sweets: chocolate > ice cream with inflation of 11.3% and 22.4%, respectively.

Other:

Clothing & footwear with 6% inflation is somewhat ok, maybe go for winter cloth shopping?

Housing is generally fine, apart from the electricity, gas & other fuels section which has skyrocketed by 57.6%! Watch out!

If you plan to do some redecorating of your home, then be aware that furniture is up 13%.

Healthcare remains ok’ish with general inflation of 6.4%, but out-patient services being up 10.8%.

Transportation: bicycles are up only 3.6%, looks kind of as a no-brainer with the energy prices?

Restaurants & hotels: if you have to pick one, then go and have some lovely dinner! Restaurant prices have increased 10.6%, while hotel pricing have jumped 34.8%!

The culprit in financial services is insurance with inflation of 36.9% in general and 43.4% related to cars. I wonder why? I wonder how?

Deflationary group:

I found a group where the price of goods have deflated aaand it’s audio-visual equipment with -7%!!! Honestly, idk what to do with this stuff, but it’s nice to see something going the other direction.

The cost of pre-primary education has gone down 9.9%! Feels unbelievable, but nice.

Summing it up

If we generalize, then we can see that price increase in services is lagging behind the goods which makes sense & unfortunately is likely to catch up as their costs are raising.

Consumer price changes:

Goods: 20.3%

Non-food goods: 24.8%

Services: 7.2%

Summary

The impact of inflation can be limited!

Understand where do you stand - what are your costs, where can you cut & what is the impact.

Don't overspend the money just because it feels like the prices will always go up. Having cash is a super power, especially, if the house is on fire.

Be smart about your spend, inflation differs for different goods & services.

Think ahead even if there are many unknowns. Planning will still help & it will definitely make you better prepared for any surprises that life throws at you.

I’m writing this to guide myself through the current events & I hope that I will manage to help others by doing that.

As usual, I am more than interested in your thoughts.

Hope for the best but be ready for the worst.