#2 Latvian house party - what does it cost to build a house?

Matīss & Fakebella continue their hustle to build a house, will they succeed? Let's find out how likely it is to happen as they go to the architect, potential construction contractor & the bank

The last time around our lovely couple managed to buy a land plot with the help of bank financing & they feel ready to take the next steps to become proud homeowners.

As we did find out the last time, then the price of the land plot matters as it might impact the financing amount available for the construction part. They started with savings of €50,000 & are left with €32,000 after buying the plot.

Let’s find out whether their current savings are sufficient to start building an actual house. They are heading to their architect next..

👩🎨 Designing & planning the actual construction

Hiring an architect

They have a friend & she even gave the green light for that land plot as there are no major limitations to building on it. This is something of great importance, as that can make everything even more complicated & believe me - you do not want that.

She is giving them a friendly price: €4,000 which would be paid in parts.

However, as it turns out, you need many more experts apart from the architect & to name a few: construction engineer, energy efficiency engineer, electrical engineer, water or wastewater engineer & interior designer (optional). Yes, they are all separate people & expect to be paid. Matīss & Fakebella decide to become interior designers, but other positions would still sum up to €3,000.

Budget at least €10,000 for this part to be on the safe side.

Understanding the construction costs

This is a super tricky part, at least for me. My understanding of an actual construction project was very limited not to say non-existent. It still is.

You will need almost finished architecture for the building to receive a quote from some potential construction companies otherwise it’s gonna be a very random guestimate. Note that it will be a guestimate anyway (a lot can change, say pandemic, war, supply chain crisis & so on..), but you want to have it at least somewhat accurate.

Ask around & find at least three potential builders. Be ready that it might cost something. Roughly €200 - €300 per quote, but sometimes they are ready to do it for free. It’s a very good idea to provide them with a similar template to be filled, as otherwise, it’s gonna be close to impossible to compare their offerings. Again, trust me.

A very important part here is that you (a) understand something about the construction, (b) have an architect that understands that or, (c) there is someone else that is helping you. Be aware of the fact that it’s pretty unlikely that you will become a construction expert in a few months.

Being too self-confident here can be very costly.

Their construction costs

Matīss & Fakebella’s quote comes in at €230,000. It’s €1,277/m2 & would be considered a very good price. It’s without furniture if you are wondering, but kind of livable.

At this point, they need to go to the real estate valuation agency once again & get the official valuation for the bank loan. Two weeks later, their lovely future home is valued at €210,000. It’s below construction cost which sucks & you will see why later on.

! IMPORTANT ! As mentioned, they will look at similar comparable deals, not the construction costs. Sure, construction costs will have some impact, but there will be no impact if your toilet is made from gold.

🧮 How does this all add up?

Their status quo

They have done some spending already & want to understand how much money they need to start building & what can they get from the bank.

So far they have spent €25,500:

land & financing related costs: €18,000

designing the mansion-related costs: €7,500

Meaning that their savings are down to €24,500 & monthly credit payments stand at €548 (together with their car lease).

Our couple goes to the bank

Fakebella takes (a) a summary of the construction quotes, (b) the official valuation & (c) their project and fills out multiple loan applications.

Their main bank that gave loan for land has the following offer:

Loan amount:

€151,500 or 80% of the future value (FV) minus the existing bank loan for the land plot. (210,000 * 0.8 - 16,500 = 151,500)

The couple's part would be €78,500, as in their case they have to look at the construction part not FV, i.e. €230k, not €210k. I mean they literally will have to build the house to get to the FV. (230,000 - 151,500 = 78,500)

Interest rate:

2.89% + Euribor until construction works are finished

2.09% + Euribor when the building is officially finished

Other very important points that the bank makes:

their part (€78,500) should be available in their bank account in the specific bank.

bank’s funding will start flowing only when their part will be spent.

bank money will not be paid out before there is a foundation & a new building status is received from the regional construction board.

the loan will be split into three payments during several construction parts.

So they are missing €54,000. (78,500 - 24,500 = 54,000)

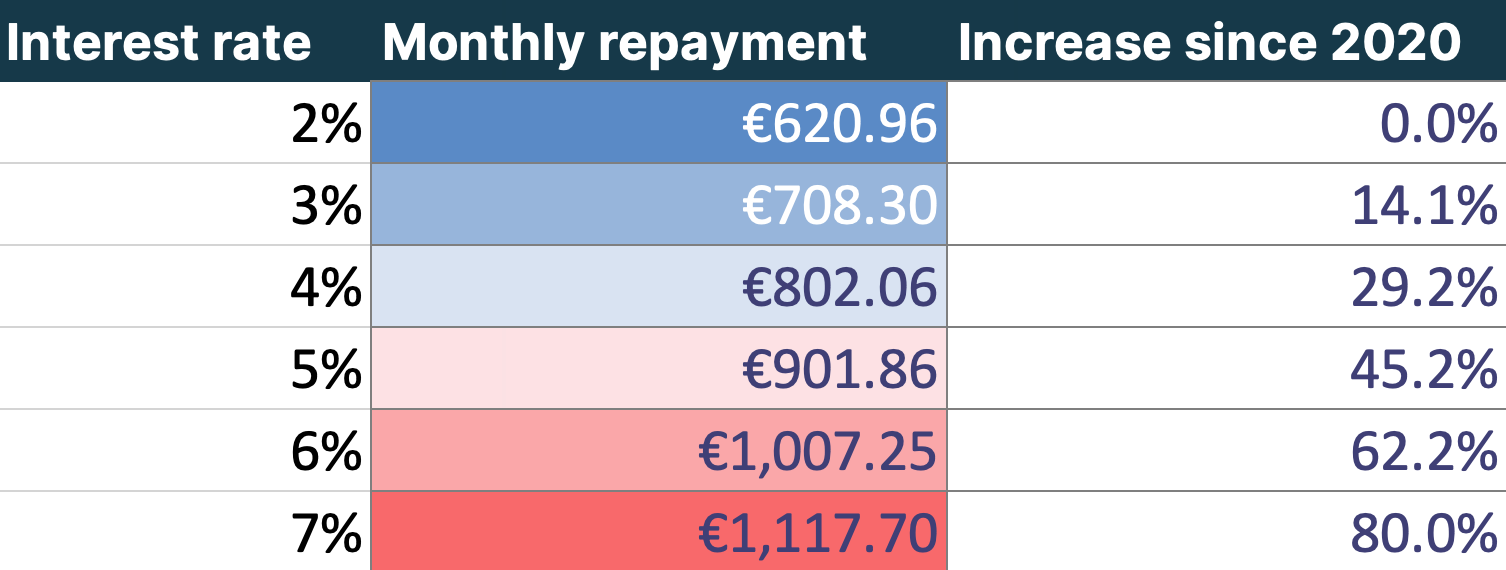

The impact of interest rates for monthly repayments

As you may or may not know, Euribor rates have changed, jumping from negative to ~3.5%, possibly rising more. Good bank clients can get a fixed part of 2% or lower, totalling 5.5% interest. It might feel like a lot, but historically speaking it’s not bad. In 2001 & 2008, the Euribor alone was above 5%, so at least 7% (it was more) in interest for a mortgage. It is extremely important that you consider this before taking a loan. Let me show why.

Here is the difference in monthly loan repayments for a 30-year, €168,000 mortgage with different rates 👇

If the rates go from 2% to 7% (not impossible), then the monthly repayment almost doubles from €620.96 to €1117.70.

Are there any alternatives for our friends?

Yes, but it, of course, has some other implications.

Altum guarantees. With the program for young specialists, it is possible to theoretically decrease the down payment to 5%. In reality though, the bank is still very likely (97%) to ask you to lay the foundations & only then give their capital. Typically, finishing the foundation costs at least €20k, if the ground quality is good, but can easily go to €30 - 50k. Furthermore, a smaller down payment means a higher monthly payment for the loan.

I.e. with Altum, bank will still ask for foundation (€20,000), leading to €190,000 loan. Monthly payment: ~€1,000 on 30-year, 5% interest mortgage. Total monthly liabilities: €1.5k (including car lease), 35% of income. Savings down to a couple of thousand.

I would strongly advise against having larger than 30% of liabilities for monthly cash flow. It will get very stressful at some point.

Work with the project. There are lots of things that can be done to optimize the costs of the project. Furthermore, there is always the option to try again with a less ambitious project. That should be the case for Matīss & Fakebella, as mentioned that they shouldn’t really go for significantly more than €1,000 in monthly liabilities alone.

Put a mortgage on another property. Please note, that the fact that it’s possible does not mean that you have to actually do it. Even though you would get additional capital, your total liabilities increase & you would need to make monthly repayments & with the current Euribor, it would be too expensive. Also, not really possible in this specific case.

Buying an already built house. It’s a lot more straightforward, as you just pay a 15% down payment & pretty much move in.

A tl;dr summary

A wonderful couple with an after-tax income of €4,200 & savings of €50,000 wants to build a house.

They buy a land plot for €33,000 that is partly (50%) financed by the bank.

Their project’s construction cost is quoted at €230,000, while the official valuation comes in at €210,000.

The bank finances 80% of the valuation minus the existing loan for the land plot, namely €151,500.

They have already spent €25,500 (land & other costs) & they will need an additional €78,500 to qualify for a bank loan.

Yet, they have only €24,500 left, meaning they must get another €54,000.

The general observation is that a household needs savings of at least €100k & €5,000 in monthly income to build a house. These amounts will still make the process rather tricky, as there of course remain risks during the actual building process, i.e. changes in material or construction prices or even the contractor going under or disappearing.

Sure. I know. This all might sound a bit gloomy. However, I believe that it is important to talk about objective reality & not give false expectations. I hope that this will be helpful as you start with your dream project.

No pun intended - the more beautiful houses the merrier!

& of course, of course, some fitting music for you to start going:

“I want a brand new house on an episode of Cribs

And a bathroom I can play baseball in..“